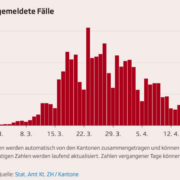

March 2020 was scary for most people around the world. A new and dangerous virus was afoot and uncertainty was the order of the day. As it turned out, for many of us we made a rapid pivot to working remotely and to social distancing.

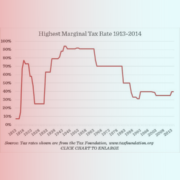

Let’s veer into the political economy today, a sort of third rail of market and economic commentary. The reason I want to discuss it is the tax grab contemplated by the Biden Administration in the US.

We arrived in Japan recently to attend to some family matters. One household issue we also wanted to deal with was our legacy washing machine. Little did I know that this would start an adventure in both technology and Economics.